The Massive Flip thesis has been gaining traction within the monetary world and describes the market’s misplaced perception within the path of inflation and coverage charges.

The article beneath is a free full piece from a current version of Bitcoin Journal PRO, Bitcoin Journal’s premium markets e-newsletter. To be among the many first to obtain these insights and different on-chain bitcoin market evaluation straight to your inbox, subscribe now.

The Massive Flip

On this article, we break down a macro thesis that has been gaining an growing quantity of traction within the monetary world. The “Massive Flip” was first launched by pseudonymous macro dealer INArteCarloDoss, and relies in the marketplace’s obvious misplaced perception on the trail of inflation and subsequently the trail of coverage charges.

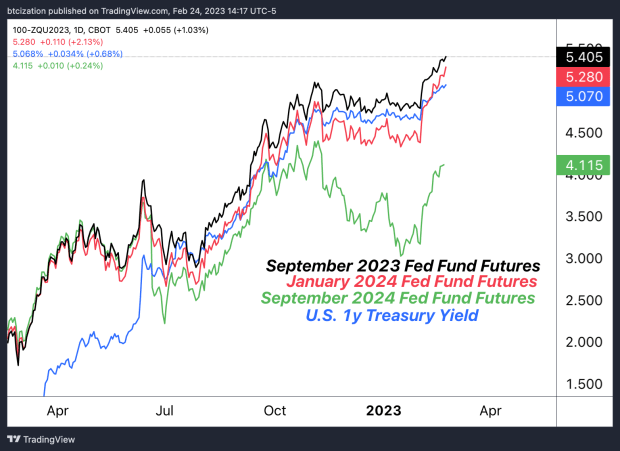

To simplify the thesis, the Massive Flip was constructed upon the idea that an imminent recession in 2023 was improper. Despite the fact that the charges market had absolutely priced within the perception that an impending recession was probably, the massive flip and recession timeline could take longer to play out. Particularly, this variation in market expectations could be seen by way of Fed fund futures and short-end charges in U.S. Treasuries.

Within the second half of 2022, because the market consensus flipped from anticipating entrenched inflation to disinflation and an eventual financial contraction in 2023, the charges market started to cost in a number of fee cuts by the Federal Reserve, which served as a tailwind for equites attributable to this expectation of a decrease low cost fee.

In “No Coverage Pivot In Sight: “Greater For Longer” Charges On The Horizon,” we wrote:

“In our view, till there may be significant deceleration within the 1-month and 3-month annualized readings for measures within the sticky bucket, Fed coverage will stay sufficiently restrictive — and will even tighten additional.”

“Whereas it’s probably not within the pursuits of most passive market members to dramatically alter the asset allocation of their portfolio primarily based on the tone or expression of the Fed Chairman, we do consider that “larger for longer” is a tone that the Fed will proceed to speak with the market.

“In that regard, it’s probably that these trying to aggressively front-run the coverage pivot could as soon as once more get caught offside, no less than briefly.

“We consider {that a} readjustment of fee expectations larger is feasible in 2023, as inflation stays persistent. This situation would result in a continued ratcheting of charges, sending danger asset costs decrease to mirror larger low cost charges.”

Because the launch of that article on January 31, the Fed funds futures for January 2024 have risen by 82 foundation factors (+0.82%), erasing over three full interest-rate cuts that the market initially anticipated to happen throughout 2023, with a slew of Fed audio system lately reiterating this “larger for longer” stance.

As we drafted this text, the Massive Flip thesis continues to play out. On February 24, Core PCE value index got here in larger than anticipated.

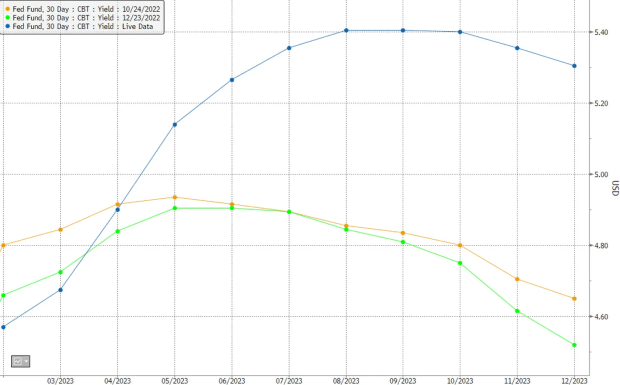

Proven beneath is the anticipated path for the Fed funds fee throughout October, December and within the current.

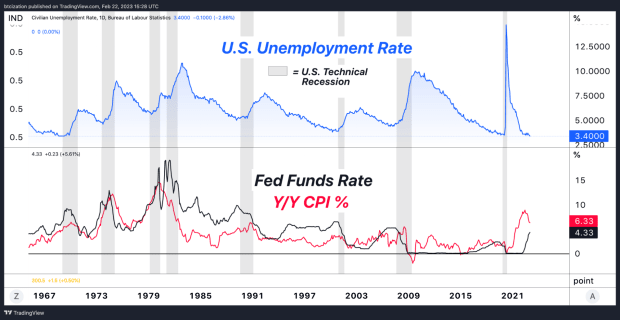

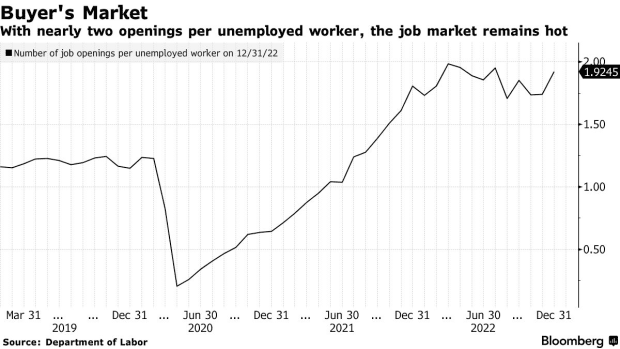

Regardless of the disinflation CPI readings on a year-over-year foundation throughout a lot of the second half of 2022, the character of this inflationary market regime is one thing that almost all market members have by no means skilled. This will result in the idea of “transitory” pressures, when in actuality, inflation seems to be entrenched attributable to a structural scarcity within the labor market, to not point out monetary situations which have significantly eased since October. The easing of economic situations will increase the propensity for customers to proceed to spend, including to the inflationary strain the Fed is trying to squash.

With the official unemployment fee in america at 53-year lows, structural inflation within the office will stay till there may be ample slack within the labor market, which would require the Fed to proceed to tighten the belt in an try to choke out the inflation that more and more seems to be entrenched.

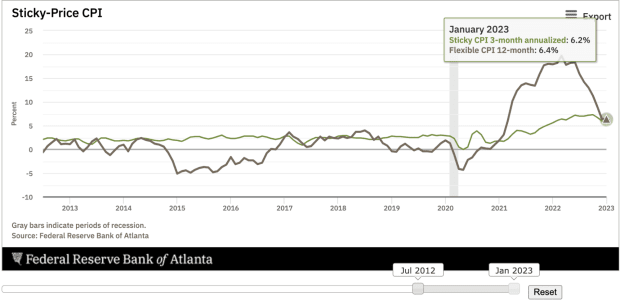

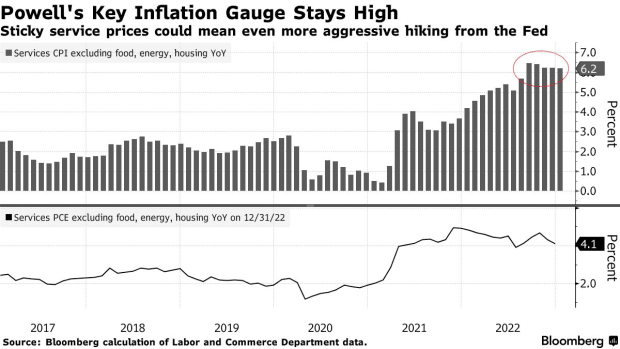

Whereas versatile parts of the buyer value index have fallen aggressively since their peak in 2022, the sticky parts of inflation — with a selected concentrate on wages within the service sector — proceed to stay stubbornly excessive, prompting the Fed to proceed their mission to suck the air out of the figurative room within the U.S. financial system.

Sticky CPI measures inflation in items and providers the place costs have a tendency to vary extra slowly. Which means that as soon as a value hike comes, it’s a lot much less more likely to abate and is much less delicate to pressures that come from the tighter financial coverage. With Sticky CPI nonetheless studying 6.2% on a three-month annualized foundation, there may be ample proof {that a} “larger for longer” coverage stance is required for the Fed. This seems to be precisely what’s getting priced in.

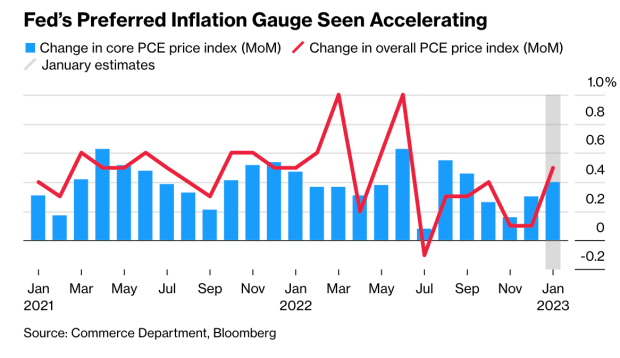

Printed on February 18, Bloomberg reiterated the stance of disinflation flipping again towards a reacceleration within the article “Fed’s Most well-liked Inflation Gauges Seen Working Sizzling.”

“It’s gorgeous that the decline in year-over-year inflation has stalled utterly, given the favorable base results and provide surroundings. Meaning it gained’t take a lot for brand new inflation peaks to come up.” — Bloomberg Economics

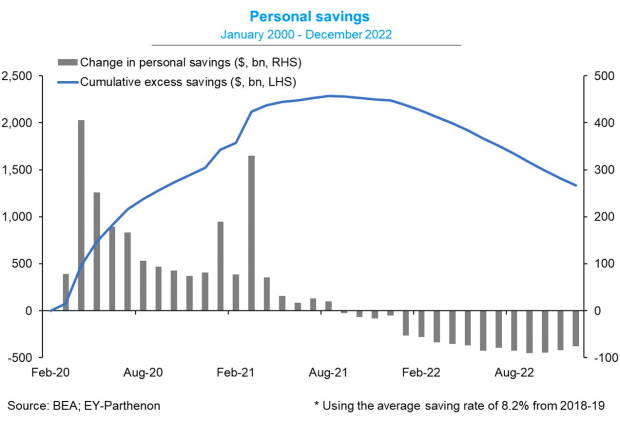

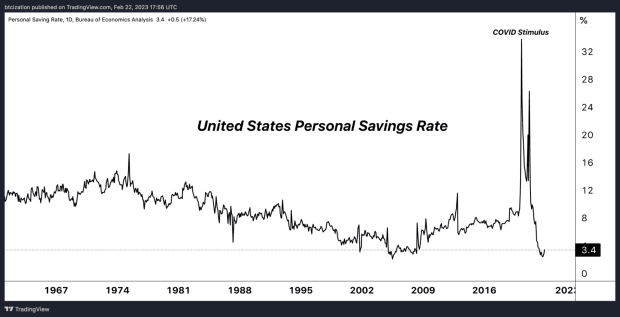

This comes at a time when customers nonetheless have roughly $1.3 trillion in extra financial savings to gas consumption.

Whereas the financial savings fee is extraordinarily low and combination financial savings for households is dwindling, the proof suggests that there’s loads of buffer to proceed to maintain the financial system piping scorching in nominal phrases in the meanwhile, stoking inflationary pressures whereas the lag results of financial coverage filter by way of the financial system.

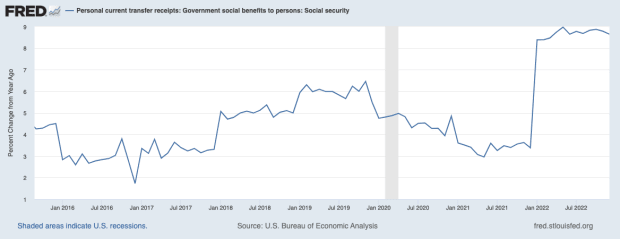

It is usually vital to recollect that there’s a part of the financial system that’s far much less rate-sensitive. Whereas the financialized world — Wall Avenue, Enterprise Capital corporations, Tech corporations, and many others. — are reliant on zero interest-rate coverage, there may be one other part of the U.S. financial system that may be very a lot insensitive to charges: these depending on social advantages.

Those that are depending on federal outlays are enjoying a big half in driving the nominally scorching financial system, as cost-of-living changes (COLA) have been absolutely carried out in January, delivering a 8.3% nominal improve in shopping for energy to recipients.

Social safety recipients are literally not in possession of any elevated shopping for energy in actual phrases. The psychology of a nominal improve in outlays is a strong one, significantly for a era not used to inflationary strain. The additional cash in social safety checks will proceed to result in nominal financial momentum.

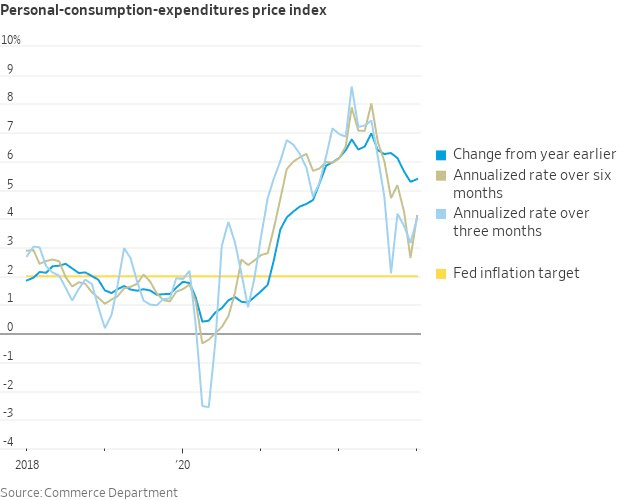

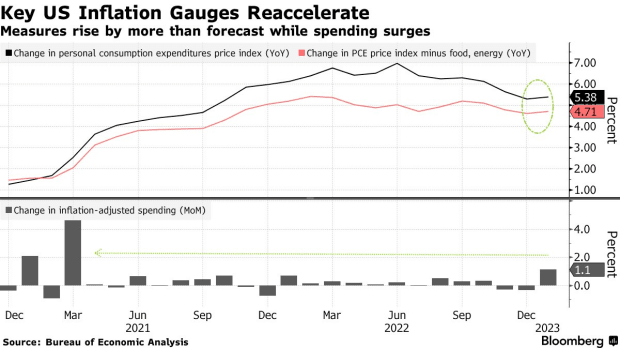

Core PCE Comes In Sizzling

In Core PCE information from February 24, the month-over-month studying was the most important change within the index since March 2022, breaking the disinflationary development noticed over the second half of the 12 months which served as a brief tailwind for danger belongings and bonds.

The recent Core PCE print is vitally vital for the Fed, as Core PCE notably carries a scarcity of variability within the information in comparison with CPI, given the exclusion of power and meals costs. Whereas one could ask in regards to the viability of an inflation gauge with out power or meals, the important thing level to grasp is that the unstable nature of commodities of mentioned classes can distort the development with elevated ranges of volatility. The actual concern for Jerome Powell and the Fed is a wage-price spiral, the place larger costs beget larger costs, lodging itself into the psychology of each companies and laborers in a nasty suggestions loop.

“That’s the priority for Powell and his colleagues, sitting some 600 miles away in Washington, and attempting to determine how a lot larger they have to elevate rates of interest to tame inflation. What Farley’s describing comes uncomfortably near what’s identified in economist parlance as a wage-price spiral – precisely the factor the Fed is set to keep away from, at any price.” —- “Jerome Powell’s Worst Concern Dangers Coming True in Southern Job Market”

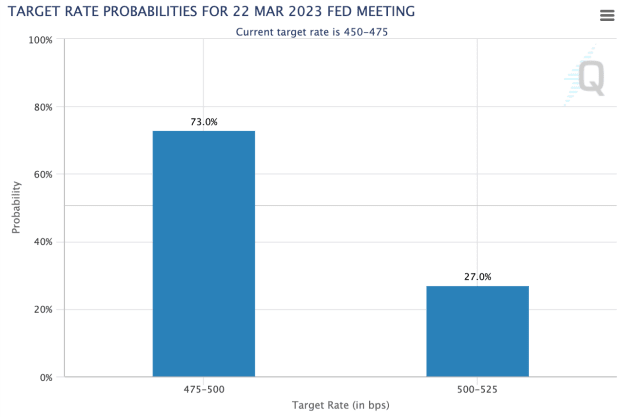

The Fed’s subsequent assembly is on March 21 and 22, the place the market has assigned a 73.0% chance of a 25 bps fee hike on the time of writing, with the remaining 27% leaning towards a 50 bps hike within the coverage fee.

The growing momentum for a better terminal fee ought to give market members some pause, as fairness market valuations more and more look to be disconnected from the reductions within the charges market.

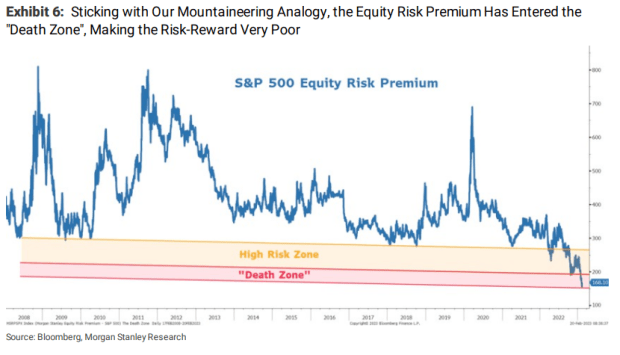

A lead Morgan Stanley strategist lately expressed this very concern to Bloomberg, citing the fairness danger premium, a measure of the anticipated yield differential given within the danger free (in nominal phrases) bond market relative to the earnings yield anticipated within the fairness market.

“That doesn’t bode effectively for shares because the sharp rally this 12 months has left them the costliest since 2007 by the measure of fairness danger premium, which has entered a degree generally known as the ‘demise zone,’ the strategist mentioned.

“The danger-reward for equities is now ‘very poor,’ particularly because the Fed is much from ending its financial tightening, charges stay larger throughout the curve and earnings expectations are nonetheless 10% to twenty% too excessive, Wilson wrote in a notice.

“‘It’s time to move again to base camp earlier than the following information down in earnings,’ mentioned the strategist — ranked No. 1 in final 12 months’s Institutional Investor survey when he appropriately predicted the selloff in shares.” — Bloomberg, Morgan Stanley Says S&P 500 May Drop 26% in Months

Remaining Observe:

Inflation is firmly entrenched into the U.S. financial system and the Fed is set to boost charges as excessive as wanted to sufficiently abate structural inflationary pressures, which is able to probably require breaking each the labor and inventory market within the course of.

The hopes of a comfortable touchdown that many subtle buyers had at first of the 12 months look to be dissipating with “larger for longer” being the important thing message despatched by the market over current days and weeks.

Regardless of being practically 20% beneath all-time highs, shares are pricier immediately than they have been on the peak of 2021 and the beginning of 2022, relative to charges supplied within the Treasury market.

This inversion of equities priced relative to Treasuries is a primary instance of the Massive Flip in motion.

Like this content material? Subscribe now to obtain PRO articles straight in your inbox.

Related Previous Articles:

- No Coverage Pivot In Sight: “Greater For Longer” Charges On The Horizon

- Decoupling Denial: Bitcoin’s Danger-On Correlations

- A Story of Tail Dangers: The Fiat Prisoner’s Dilemma

- A Rising Tide Lifts All Boats: Bitcoin, Danger Belongings Leap With Elevated World Liquidity

- On-Chain Knowledge Exhibits ‘Potential Backside’ For Bitcoin However Macro Headwinds Stay

- PRO Market Keys Of The Week: 2/20/2023

from Bitcoin – My Blog https://ift.tt/h2Kjw4U

via IFTTT

No comments:

Post a Comment